Wells Fargo: Overall Investor Optimism Dips in First Quarter, Black and African American Investors Signal Brighter Outlook Ahead

Even so, one in three Black and African American investors (31%) still say that the pandemic has had a negative impact on their finances

SAN FRANCISCO–(BUSINESS WIRE)–U.S. investor optimism dipped in the first quarter as unimagined turmoil roiled the nation’s capital and confusion and delays in the administration of COVID-19 vaccines captured public attention.

The Wells Fargo/Gallup Investor and Retirement Optimism Index fell to +26, down 16 points from +42 in Q4. This reversed much of the improvement seen in the fourth quarter as the markets surged following positive news about COVID-19 vaccine trials.

The dip in optimism this quarter was in part due to investors being less optimistic about their household income. Within the index, investors’ 12-month outlook for inflation dropped the most this quarter. Slight declines were also seen in their positive forecasts for unemployment, the stock market and economic growth. At the same time, investors’ outlooks for reaching their investment goals were steady.

“The COVID-19 pandemic and ensuing economic and market downturn in 2020 tested investors’ resolve, but patience and resiliency were key in helping them weather the ongoing storm,” said Veronica Willis, investment strategy analyst for Wells Fargo Investment Institute.

The Wells Fargo/Gallup Investor and Retirement Optimism Index included U.S. adults with $10,000 or more in investible assets. The first quarter poll was conducted Feb. 8-16 with 1,536 investors, including 573 Black and African American investors weighted to their correct proportion of the U.S. investor population. This oversample was designed to allow for robust analysis of Black and African American investors’ views on a range of financial topics.

While Black and African American investors reported higher optimism, some cited negative impact on finances

Despite the downtick in overall investor optimism, Black and African American investors’ overall optimism score was +101, significantly higher than the national average. Even so, one in three (31%) still said that the pandemic has had a negative impact on their finances.

About one in six Black and African American investors (17%) said that their current income equals their expenses and one in eight reported they are either drawing on savings (10%) or running into debt (3%). Nevertheless, seven in 10 reported being able to save a little (53%) or a lot (17%).

Fifteen percent of Black and African American investors who have a retirement plan reported taking a loan from their 401(k) or similar type of personal retirement plan since the start of the pandemic.

Nine percent of all investors took such a loan and among this group, the primary reason they cited for tapping their retirement funds was to pay off debt (35%). This was followed by 21% saying they used it to pay for a major expense, such as medical bills, and 16% said to help pay for their normal daily expenses. Another 18% said they used it to make a major purchase of some kind while 4% used it to help other family members.

“While certain communities continue to be disproportionately impacted by COVID-19, I believe the significantly higher optimism of Black and African American investors signals that they see a light at the end of the tunnel,” said David Dawkins, director of Diverse Client Segments at Wells Fargo Advisors.

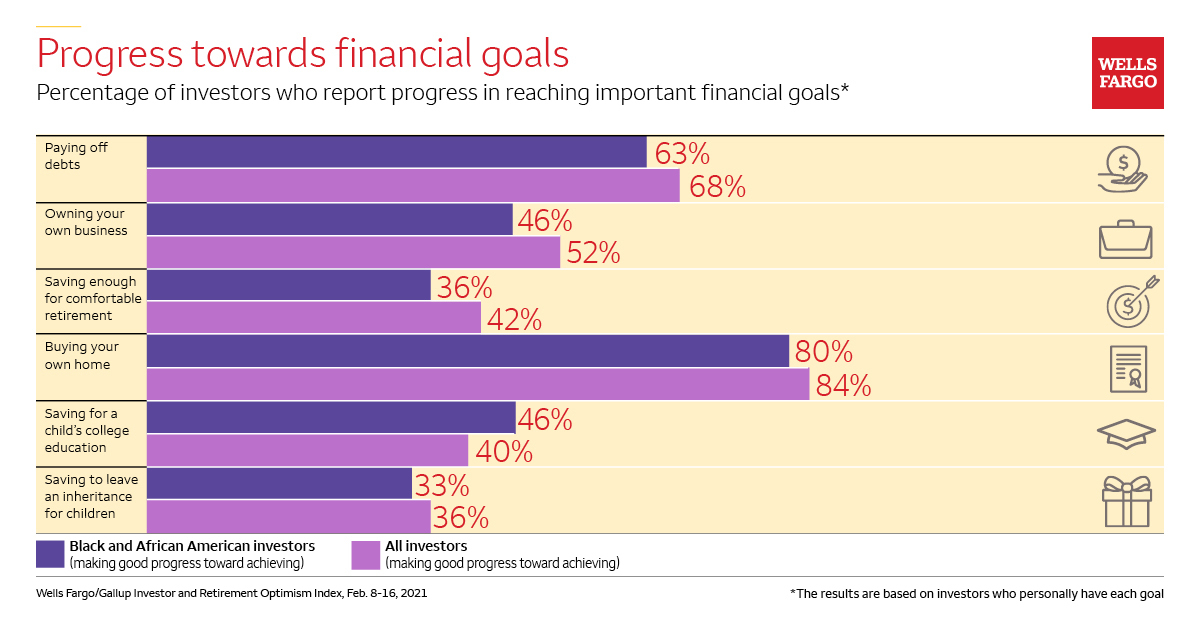

Black and African American investors reported similar progress in reaching financial life goals

Looking at Black and African American investors’ long-term financial health, nearly all (87%) Black and African American investors reported having a retirement savings plan (similar to 89% among all investors). Additionally, Black and African American investors reported similar progress with respect to other financial goals.

The poll asked investors to rank and describe how much progress they have made on six financial-oriented life goals. Progress toward achieving these goals was only slightly lower among Black and African American investors, with the exception of saving for a child’s college education where Black and African American investors slightly outpaced all investors.

- Paying off debts (63% of Black and African American investors vs. 68% of all investors)

- Owning your own business (46% vs. 52%)

- Saving enough to live comfortably in retirement (36% vs. 42%)

- Buying your own home (80% vs. 84%)

- Saving for a child’s college education (46% vs. 40%)

- Saving to leave an inheritance for your children (33% vs. 36%)

“Although the data indicates similar progress in achieving financial goals, it still shows an alarming number of investors who are not reporting strong progress toward achieving their goals — particularly the goals with a longer time horizon,” said Dawkins.

Black and African American investors are more risk averse with investments

Seventy-two percent of Black and African American investors said they believe the stock market is a good place for people to invest and grow their retirement savings. However, when asked about their risk tolerance in investing, 38% of Black and African American investors said they are willing to take on “a lot” or “fair amount” of risk as compared to 47% of all investors. Instead, the majority of Black and African American investors (54%) said they are willing to take “only a little” risk.

This gap in risk tolerance is mainly explained by lower risk tolerance among Black and African American men. Black and African American male investors (44%) are less willing to take a lot or fair amount of risk with their investments than all male investors (55%). There is little difference by race in risk tolerance among females (35% of Black and African American female investors vs. 39% of all female investors).

“While the data still affirms that men tend to be more aggressive investors than women, the racial divide among male investors adds a new layer of complexity,” said Dawkins. “People of color already face additional earnings barriers. Taking on too much or too little risk can perpetuate this. Investors should ensure that their risk tolerance is aligned to their investment objectives to help maximize achieving their goals.”

Black and African American investors give and receive family financial support

Having access to financial support from family was a sentiment shared by all investors. However, Black and African American investors are more likely to have received such help. Twenty-two percent of all Black and African American investors said they have personally received financial help from a family member or friend in the past few years (vs. 15% of all investors).

Black and African American investors indicated that family financial support is a two-way street, with 69% of this group saying they have provided significant or routine financial help to at least one family member or friend in the past few years compared to 57% of all investors.

When asked to estimate how much money has been given in the past few years, Black and African American investors reported approximately $17,000 as compared to about $25,000 for all investors.

Black and African American investors who are parents prioritize educating their children on finance

Most Black and African American investors with adult children said they provided a lot or a fair amount of education to their children about handling finances — such as earning, saving, budgeting, borrowing, donating and investing money. In fact, Black and African American investors were six percentage points more likely than all investors to have done so (84% of Black and African American investors vs. 78% of all investors).

By contrast, far fewer Black and African American investors reported that their own parents provided a lot or a fair amount of financial education to them growing up (33%).

And despite doing more than their parents to educate their own children on finances, 41% of Black and African American investors think they should have provided more financial education to their children.

“The idea of closing the wealth gap is important to Black and African American parents who invest,” said Dawkins. “They know that income and wealth parity starts with strong financial acumen and education — and are choosing to tackle that head on.”

About the Wells Fargo/Gallup Investor and Retirement Optimism Index

Results for this Wells Fargo/Gallup Investor and Retirement Optimism Index are based on a Gallup Panel™ web study completed by 1,536 U.S. investors, aged 18 and older, from Feb. 8-16. This quarter’s poll includes an oversample of Black and African American investors, resulting in a total of 573 Black and African American investors included in this survey.

The Gallup Panel is a probability-based, longitudinal panel of U.S. adults who Gallup selects using random-digit-dial phone interviews that cover landline and cellphones. Gallup also uses address-based sampling methods to recruit Panel members. The Gallup Panel is not an opt-in panel. The sample for this study was weighted to be demographically representative of the U.S. investor population, using demographic targets determined from investor samples within prior Gallup national adult surveys. For results based on this sample, one can say that the maximum margin of sampling error is ±4 percentage points at the 95% confidence level. Margins of error are higher for subsamples. For results based on the over sample of Black and African American investors, one can say that the maximum margin of sampling error is ±6 percentage points at the 95% confidence level.

In addition to sampling error, question wording and practical difficulties in conducting surveys can introduce error and bias into the findings of public opinion polls.

For this study, the American investor is defined as an adult in a household with stocks, bonds or mutual funds of $10,000 or more, either in an investment account or in a self-directed IRA or 401(k) retirement account. About two in five U.S. households have at least $10,000 in such investments. The sample consists of 58% nonretirees and 42% retirees. Of total respondents, 39% reported annual incomes of less than $90,000; 57% reported $90,000 or more. The median age of the nonretired investor is 47 and the retiree is 68. The Wells Fargo/Gallup Investor and Retirement Index is an enhanced version of Gallup’s Index of Investor Optimism, which provides the historical trend data.

The Investor and Retirement Optimism Index has an adjusted baseline score of 100 from when it was established in October 1996. It peaked at +152 in January 2000, at the height of the dot-com boom, and hit a low of -81 in February 2009.

About Wells Fargo

Wells Fargo & Company (NYSE: WFC) is a diversified, community-based financial services company with $1.9 trillion in assets. Wells Fargo’s vision is to satisfy our customers’ financial needs and help them succeed financially. Founded in 1852 and headquartered in San Francisco, Wells Fargo provides banking, investment and mortgage products and services, as well as consumer and commercial finance, through 7,400 locations, more than 13,000 ATMs, the internet (wellsfargo.com) and mobile banking, and has offices in 32 countries and territories to support customers who conduct business in the global economy. With approximately 260,000 team members, Wells Fargo serves one in three households in the United States. Wells Fargo & Company was ranked No. 30 on Fortune’s 2020 rankings of America’s largest corporations. News, insights and perspectives from Wells Fargo are also available at Wells Fargo Stories.

Additional information may be found at www.wellsfargo.com | Twitter: @WellsFargo.

|

Investment and insurance products: |

||||

|

NOT FDIC-Insured |

NO Bank Guarantee |

MAY Lose Value |

||

Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC, Member SIPC, a registered broker-dealer and non-bank affiliate of Wells Fargo & Company.

Wells Fargo Investment Institute, Inc. is a registered investment adviser and wholly owned subsidiary of Wells Fargo Bank, N.A., a bank affiliate of Wells Fargo & Company.

News Release Category: WF-ERS

Contacts

Media

Jackie Knolhoff, 314-346-7670

Jackie.knolhoff@wellsfargoadvisors.com

Desari Mueller, 314-327-9615

desari.mueller@wellsfargoadvisors.com