Financed Emissions: Why They Matter, and How Financial Institutions Can Reduce Them

By Sundeep Reddy Mallu, Head of ESG and Analytics at Gramener

Compared to the mining or oil and gas industries, the financial sector might not seem like a significant contributor when it comes to greenhouse gas (GHG) emissions. But the truth is, due to their involvement in lending to the original emitter (e.g., fossil fuel companies), financial institutions are responsible for financed emissions—which are 700 times more than their directly generated emissions.

In a nutshell, financed emissions are indirect GHG emissions, also known as Scope 3 GHG emissions, caused by some financial activities such as unlisted equity, mortgages, underwriting, and business loans. To illustrate this, the world’s 60 largest banks financed up to $4.6 trillion in fossil fuels between 2015 and 2021.

But the winds of change have begun to blow: As the awareness of the critical role that financial organizations play in climate transition increases, we are witnessing more institutions stepping in to take action. For example, in 2022, Vancity became the first financial institution in Canada to set targets for reducing financed emissions in commercial and residential real estate.

Let’s dive deeper into why financial institutions need to start managing their financed emissions and how they can achieve their net-zero and decarbonization goals.

Addressing Financed Emissions Is Becoming Crucial in the Financial World

First and foremost, reducing financed emissions is slowly becoming a regulatory requirement. In the US, for instance, the Securities and Exchange Commission (SEC) put forth new regulations last year that would mandate companies to disclose climate-related information in their business reports and registration statements.

Gary Gensler, the chairperson of SEC, stated, “I am pleased to support today’s proposal because, if adopted, it would provide investors with consistent, comparable, and decision-useful information for making their investment decisions, and it would provide consistent and clear reporting obligations for issuers.”

Disclosing and managing financed emissions also enables financial institutions to get ahead of any potential risks. Consider a bank lending money to emissions-intensive portfolio companies that are profitable now but are not taking any steps to reduce emissions. Over a period of time, rising carbon taxes or caps on emissions imposed by regulators could adversely affect the financial overall of these businesses while weakening the bank’s profitability.

Added to that, organizations must take climate action seriously, especially in a world where Gen Z and millennials create a massive demand for sustainable brands and low-carbon products. Being transparent about financed emissions can help financial establishments build trust with their stakeholders, leading to an increase in customer activity, brand loyalty, and revenue.

Measuring Financed Emissions Is the First Step Forward

Even though numerous banks have pledged to make their portfolios net-zero by 2050 or sooner, only a few of them have begun to measure their financed emissions. But bear in mind that financial institutions can only make data-based decisions and design more effective strategies to reduce emissions when they collect critical information about their financed emissions.

To achieve this goal, banks can join the Partnership for Carbon Accounting Financials (PCAF). The PCAF is a global initiative seeking ways to promote transparency and help financial institutions disclose all GHG emissions resulting from investments or loans.

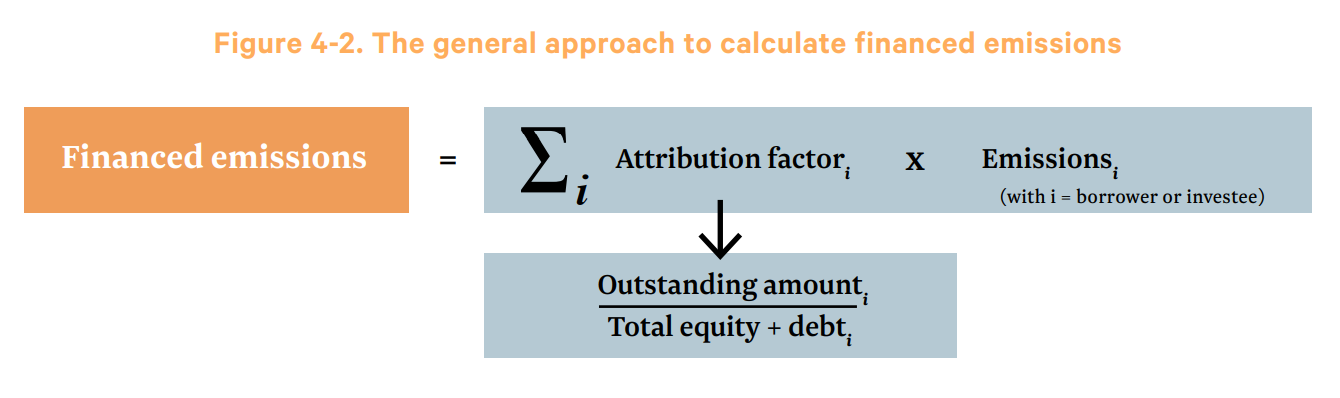

Depending on the type of asset, the amount of emissions, and the financial data available, the PCAF method for calculating emissions varies. But the figure below can show the general approach to assessing financed emissions.

Source: The Global GHG Accounting and Reporting Standard for the Financial Industry.

Thanks to this formula and the PCAF’s methods, businesses can make sure that their investment portfolio aligns with their net-zero goals and sustainability endeavors.

Best Practices to Tackle Financed Emissions

Financial institutions can take a powerful step towards reducing their financed emissions by increasing lending and investment in green technologies or eco-friendly projects. This way, they can make a real impact on the environment and their bottom line.

Virgin Money, for example, has set a target to offer £200m green loan to help farmers decarbonize their farms through actions like installing renewable energy systems such as wind turbines and solar panels.

Another prime way of reducing financed emissions is to reallocate resources. Instead of investing or lending to emission-intensive industries like fossil fuels and coal mining, banks can finance nature-based emission removal solutions while increasing exposure to climate action and sustainable development.

Banks can also look to incorporate sustainable finance instruments into their investment portfolio. Take a sustainability-linked bond, for instance. It is a type of debt instrument that requires issuers to report their sustainability performance regularly. According to their performance, financial organizations can adjust the interest rate or offer them an incentive, allowing both parties to exceed sustainability targets and improve their reputation.

Due to their investment and lending decisions, banks generate financed emissions, which are far higher than their direct ecological impact. But the rising environmental awareness and upcoming regulations are forcing them to manage their GHG emissions, improve their operations, and contribute to a cleaner future.